Do any of the following phrases sound familiar to you?

“Retirement is still a long way off. There’s plenty of time to save for it.”

“I have too many expenses right now to put anything aside.”

“I’ll get around to saving … sooner or later.”

It is common for people to feel this way about retirement savings. But it is never too early to start investing for your future. The sooner you start, the easier your path may be.

To illustrate my point, read the following example scenario.

Example Scenario

Mira is a 22-year-old recent college graduate who is thinking about investing. She recently got a job as a marketing associate at an advertising agency. Mira earns around $61,372 a year and wants to invest 10% of her income on a yearly basis until her projected retirement in 45 years. She expects to earn an average of 8% in the long-run.

Currently, she does not have any investments. Since Mira is new to investing, she makes an appointment with Kenny, her local financial advisor, to get more information. At the meeting, she gives Kenny this information so he can approximate how much she will earn given her assumptions. She also wants to know how much she will have if she waits to start investing.

Kenny provides the following analysis.

Analysis

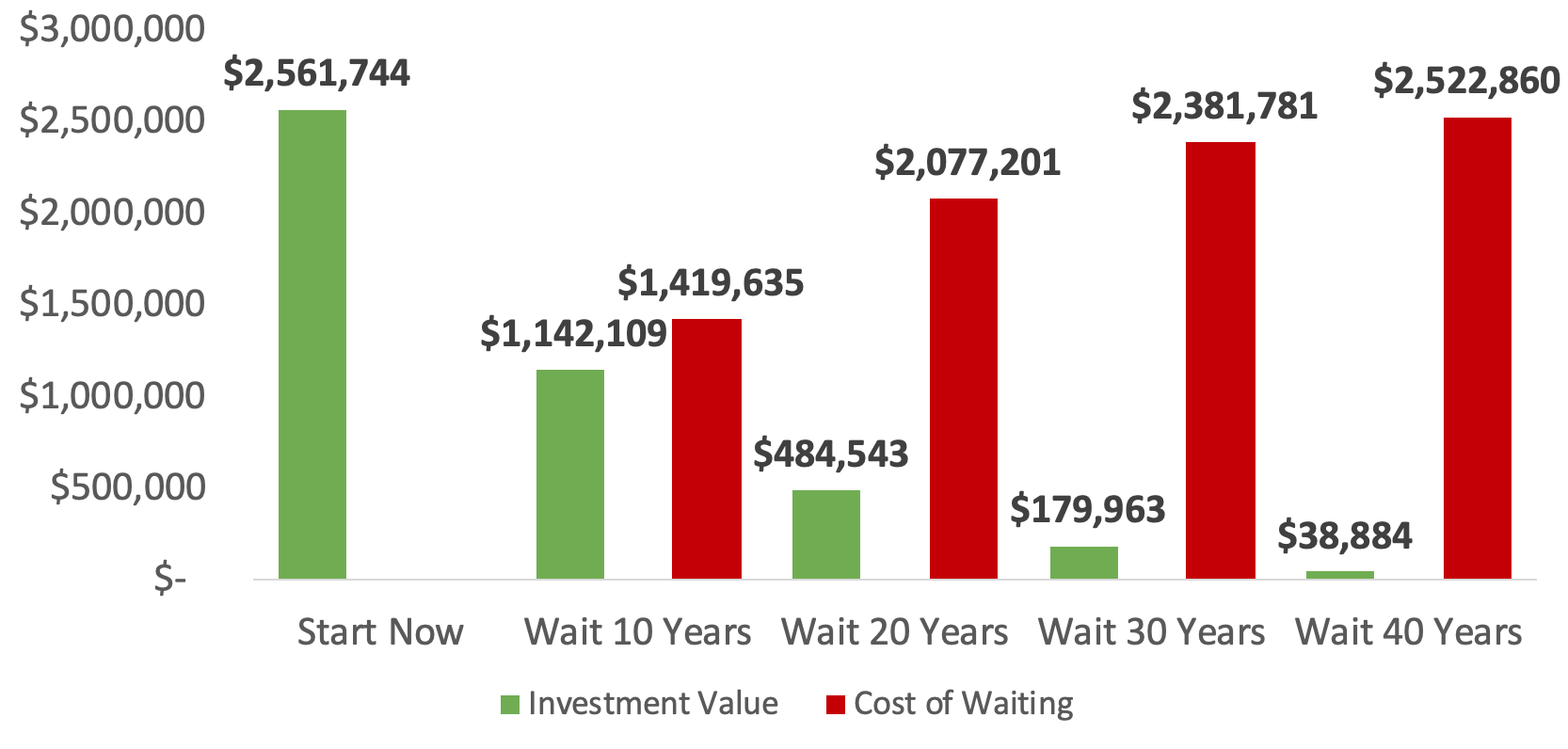

If Mira starts investing immediately, given her assumptions, she would have $2,561,744 by the time she retires. Notice, if she waits 10, 20, 30, or 40 years to begin investing, her total balance goes down significantly.

This point becomes more obvious when you change the format of the graph. If Mira decides to wait to invest, most of the damage happens in the first few years. For example, if Mira waits 10 years to invest, the opportunity cost is $1,419,635.

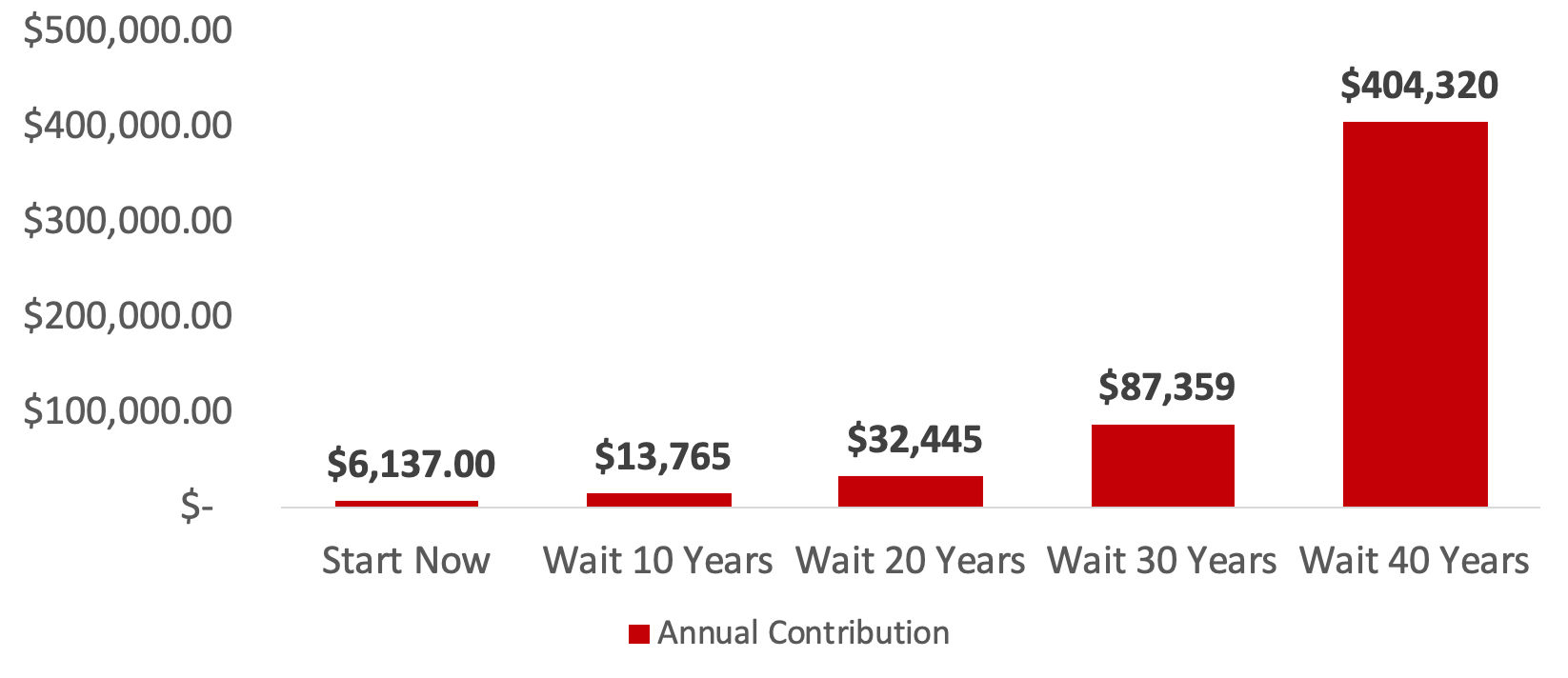

It is difficult to catch up as well. Assume Mira waits to invest but still wants to have $2,561,744 at retirement. She has two choices. Either invest more money on a yearly basis or increase the risk of her portfolio in the hopes of a earning a higher return.

If she waits 10 years, she would need to invest $13,765 annually using the same assumptions. As seen in the graph below, the longer she waits, the more expensive it is for her to attain her goal.

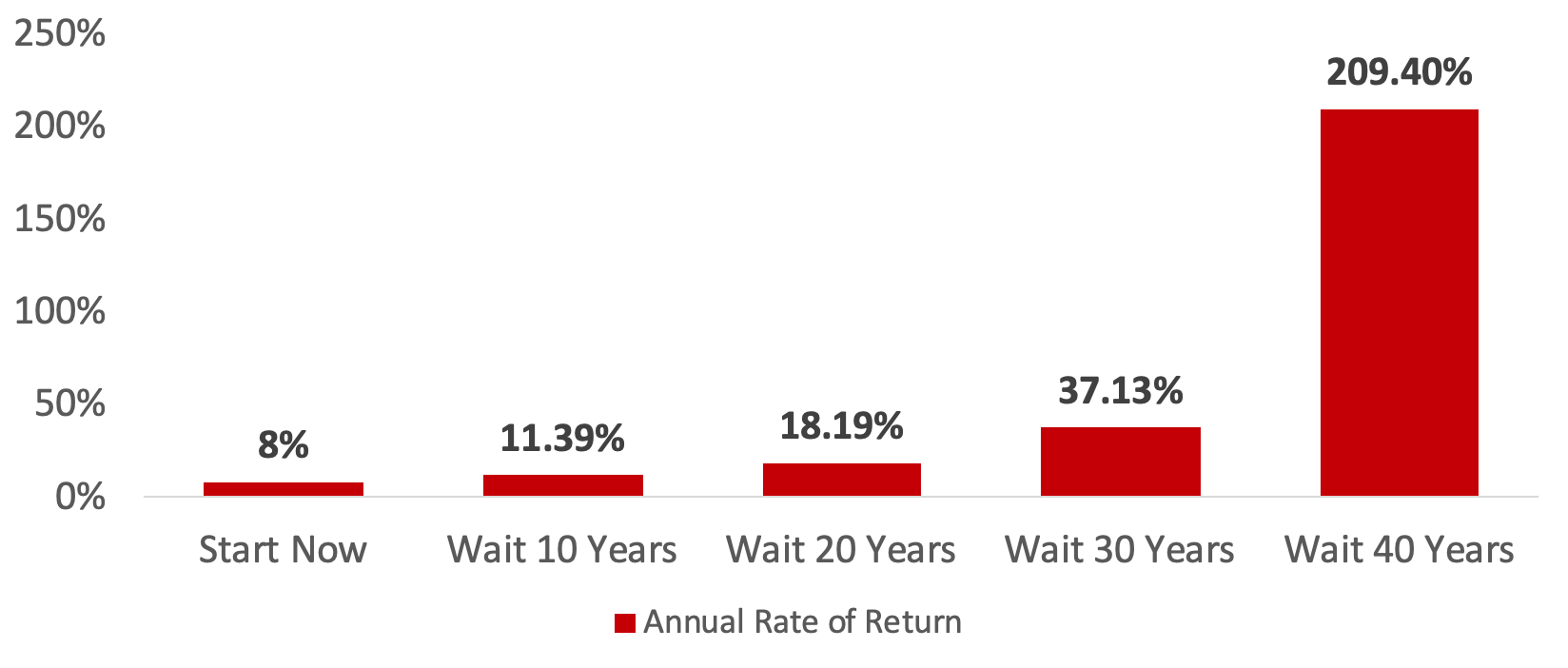

If she waits 10 years, she would need to earn an annual average rate of return of 11.39% using the same assumptions. In my opinion, I do not believe an investor can earn more than 8% on average over the long-run in a properly diversified portfolio. As seen in the following graph, the required rate of return becomes enormous.

Conclusion

When you are young and money is scarce, saving for retirement is probably the last thing on your mind. You might mistakenly assume that once you get your dream job, you will be able to make up for lost time (and money).

The truth is you will end up spending more to save less in the long-run.

Your financial situation may be different than Mira’s assumptions in my example scenario, but the general principles remain the same. It pays to start early as the cost of waiting can be catastrophic for your retirement.

Saving money is not complicated but it is one of the hardest things you will do. This is because we all have an emotional bond with money. Therefore, I believe it is important to seek out the help of a financial advisor in order to make sure you are on the right path.